There Will Be a Tomorrow #27

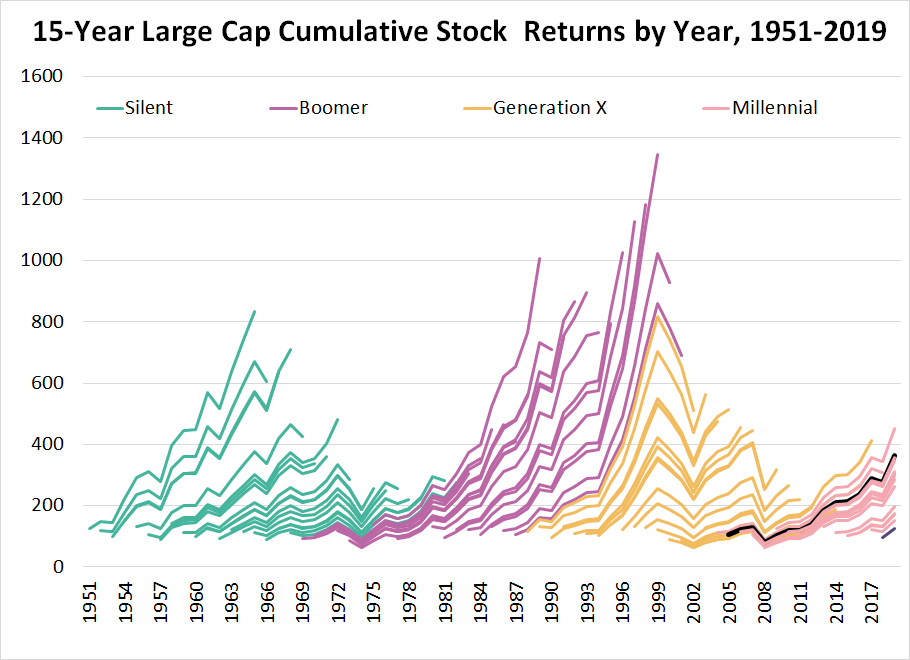

The oldest millennial will turn 40 years old on January 1st. Millennials are the generation that entered the job market as the Great Financial Crisis started and was hit by the virus when they were supposed to enter earnings peak. In the United States, millennials are one of the unluckiest generations in terms of equity returns, and that assumes that they have had enough earnings to purchase equities to begin with.

More representative of assets held by the middle classes around the World, the returns of residential property and pension funds have been paltry and correlated over the last 15 years. Housing, the traditional silver bullet to middle classes finances seems to offer similar returns to pension funds. At the same time, socialized capital has been depleted, as evidenced by the lack of physical capacity to deal with the virus. Nobody can predict the future, and hopefully things will improve over the next 15 years, but most likely millennials will have to eat their houses’ bricks or work until they die, or a combination of both.

Chile is a plausible version of the future. Thirty years ago, the Andean country fully privatized its pension system and bet everything on the mediocrity of its pension fund managers. Two years ago, middle classes suddenly realized that they would have no money to live on when they retire and burned the country’s capital. And that was before the virus hit: over the last 9 months, the Chilean government has twice allowed savers to withdraw money from their pension funds to figure the pandemic out. Last night, the Chilean central bank announced that it expects to intervene in markets to deal with the upcoming liquidity crunch. The country will likely adopt the first woke constitution in the world.

The politics of wealth redistribution will get weirder from here. Chile is a pretty unique case, and wealthy countries with a social welfare tradition will probably manage the expected pauperization of its middle classes either through the adoption of some form of capital taxation, by passing the buck on to the Gen-Zers through public debt, or a combination of both. God only knows what will happen with developing economies without a real social safety net like the United States.

While middle classes struggle, the World is probably living one of the most exciting moments in technological progress in history:

We are injecting human gens into monkeys and turning them smarter!

Singapore is commercializing lab-grown meat, which is one more step to lab-grown human organs!

Big Tech, biotech, and pharma are figuring digital medicine out, and that will be great for humanity but terrible for inequality. The potential returns to digital medicine are incredible, and the entire virus saga is a testimony to that: there’s a meme a 20 billion investment in virus classification might have saved 20 trillion to the World economy, which should give an idea of the orders of magnitude we are talking about. The asset owning class will probably get an upgrade to transhumanism. If you think that they will be deterred by the ethical considerations of college professors, you do not know anything about the asset owning class, or capitalism in general.

We would not be surprised if, over the next 20 years, the old millennials that bought into the entire experience economy thing and the ESG ideology will push into the mainstream movements that today sound as exotic as ecofascism or cyborg socialism.

Notes on the graphs:

The chart is built using the CFA Institute’s SBBI Database. The series shown is what the authors of the database calls large cap, which roughly corresponds to the S&P 500. The dark line in the millennial group represents the asset accumulation of a person born in 1982, which is the birth year of the median American by age. We referred to SBBI and looked and comparative asset accumulation by cohort for the first time here.

The table picks pension returns from the OECD 2019 “Pensions at a Glance” and housing prices from the BIS database. Both pieces of data are problematic. Pensions t a glance takes returns data as reported from pension funds, which is probably an overestimation, but if anything that bolsters our point: returns of pension funds around the World are low. Housing price indices are fundamentally appraisals or estimates derived from previous sales of similar properties.

The data on beds per 1,000 inhabitants comes from several sources. We have referred to it here and here.